кіјмҶҢнҸүк°ҖмҷҖ мҳӨн•ҙлҘј л°ӣкі мһҲлҠ” лҜёкөӯ кІҪм ңмқҳ м Җл Ҙ

By Global Trends Editor Group

мөңк·јмқҳ нҳјлһҖм—җлҸ„ л¶Ҳкө¬н•ҳкі лҜёкөӯмқҖ м—¬м „нһҲ м„ёкі„м—җм„ң к°ҖмһҘ л¶Җмң н•ҳкі м—ӯлҸҷм Ғмқё кІҪм ң лҢҖкөӯмқҙлӢӨ.

м„ нғқм—җ л”°лқј, лҜёкөӯмқҖ м—¬м „нһҲ көӯлҜјл“Өм—җкІҢ м „ м„ёкі„ мөңкі мқҳ мӮ¶мқҳ м§Ҳмқ„ м ңкіөн• мҲҳ мһҲлӢӨ.

к·ёл ҮлӢӨл©ҙ мҡ°л Өмқҳ мӢңм„ мқ„ л°ӣкі мһҲлҠ” нҳ„мһ¬ лҜёкөӯмқҳ л¶Җмұ„ мң„кё°, кІҪм ңм„ұмһҘ, мҶҢл“қкіј л¶Җмқҳ л¶ҲнҸүл“ұмқҳ л¬ём ңлҘј м–ҙл–»кІҢ н•ҙм„қн•ҙм•ј н• к№Ң?

мҳӨн•ҙлҘј л°ӣкі мһҲлҠ” лҜёкөӯ кІҪм ңмқҳ м Җл Ҙмқ„ н•ҙл¶Җн•ҙліҙмһҗ.

н…”л Ҳл№„м „мқҙлӮҳ мӣ”л“ңмҷҖмқҙл“ңмӣ№(World Wide Web)мқ„ нҶөн•ҙ, мҶҢмң„ м „л¬ёк°Җл“Өкіј м •м№ҳмқёл“Өмқҙ лҜёкөӯ кІҪм ңм—җ лҢҖн•ҙ лӢӨмқҢкіј к°ҷмқҖ 6к°Җм§Җ лҸ„л°ңм Ғ мЈјмһҘмқ„ нҺјм№ҳкі мһҲлӢӨ.

вҖңлҜёкөӯмқҳ кІҪм ңм„ұмһҘмқҙ мҡ©лӮ©н• мҲҳ м—ҶлҠ” мҲҳмӨҖмңјлЎң л‘”нҷ”лҗҳм—ҲлӢӨ.вҖқ

вҖңмҶҢл“қ л¶ҲнҸүл“ұмқҙ лҶҖлқјмҡҙ мҶҚлҸ„лЎң кі„мҶҚ кі мЎ°лҗҳкі мһҲлӢӨ.вҖқ

вҖңл¶Җмұ„ мҲҳмӨҖмқҙ кҙҖлҰ¬н•ҳкё° м–ҙл Өмҡё м§ҖкІҪм—җ мқҙлҘҙл ҖлӢӨ.вҖқ

вҖңмғқмӮ°м„ұкіј л…ёлҸҷмһҗ мһ„кёҲ к°„ м—°кІ°мқҙ лҒҠм–ҙмЎҢлӢӨ.вҖқ

вҖңл…ёлҸҷмһҗ мһ„кёҲмқҖ мҲҳмӢӯ л…„ лҸҷм•Ҳ м •мІҙлҗҳм—ҲлӢӨ.вҖқ

вҖңкі„мёө мғҒмҠ№мқҖ мқҙм ң кіјкұ°мқҳ мқјмқҙ лҗҳм—ҲлӢӨ.вҖқ

лӢЁлҸ„м§Ғмһ…м ҒмңјлЎң л§җн•ҳмһҗл©ҙ мқҙлҹ¬н•ң мЈјмһҘмқҖ мқјл¶Җмқҳ мӮ¬мӢӨм—җ кё°л°ҳн•ҳкі мһҲлӢӨ.

л¬јлЎ мқҙлҹ¬н•ң л¬ём ңл“Өмқ„ н•ҙкІ°н•ҳм§Җ м•Ҡкі л°©м№ҳн• кІҪмҡ° н–Ҙнӣ„ мҲҳ л…„ лӮҙ лҜёкөӯмқҳ н•өмӢ¬ кІҪмҹҒ мҡ°мң„к°Җ м•Ҫнҷ”лҗ мҲҳлҠ” мһҲлӢӨ.

лӢӨл§Ң мқҙлҹ¬н•ң мЈјмһҘл“Өкіј мӢӨм ң нҳ„мӢӨ мӮ¬мқҙм—җлҠ” к°„кІ©мқҙ мһҲлӢӨ.

мҷң мқҙлҹ¬н•ң мЈјмһҘмқҙ л°ңмғқн–Ҳкі , мҷң лҜёкөӯ кІҪм ңм—җ лҢҖн•ң мӢ лў° м Җн•ҳлЎң мқҙм–ҙм§Җкі мһҲлҠ”м§Җ н•ң лІҲ мӮҙнҺҙліҙмһҗ.

лЁјм Җ вҖңлҜёкөӯмқҳ кІҪм ңм„ұмһҘмқҙ мҡ©лӮ©н• мҲҳ м—ҶлҠ” мҲҳмӨҖмңјлЎң л‘”нҷ”лҗҳм—ҲлӢӨвҖқлҠ” мЈјмһҘмқ„ ліҙл©ҙ, мқҙ мқёмӢқмқҖ л¶Җ분м ҒмңјлЎң м •нҷ•н•ҳлӢӨ.

кёҲмңө мң„кё°к°Җ мӢңмһ‘лҗң нӣ„ лҜёкөӯмқҳ мӢӨм§Ҳ GDP м„ұмһҘмқҖ мһҘкё°м ҒмңјлЎң м—°к°„ 3.1%м—җм„ң 2.1%лЎң л‘”нҷ”лҗҳм—ҲлӢӨ.

мқҙлҠ” м—ӯмӮ¬м ҒмңјлЎңлҠ” л¶Җ진н•ң м„ұм ҒмқҙлӢӨ. н•ҳм§Җл§Ң лҜёкөӯ кІҪм ңлҠ” м§ҖлӮң 15л…„ лҸҷм•Ҳ 82%лӮҳ м„ұмһҘн–ҲлӢӨ.

нҶөмғҒм ҒмңјлЎң м„ұмһҘмқ„ м–ёкёүн• л•Ң л“ұмһҘн•ҳлҠ” мҡ©м–ҙлҠ” мғқмӮ°лҹүмқҙлӢӨ. мғқмӮ°лҹүмқҖ вҖҳл…ёлҸҷмӢңк°„вҖҷкіј вҖҳмӢңк°„лӢ№ мғқмӮ°м„ұвҖҷмңјлЎң кІ°м •лҗңлӢӨ.

м„ұмһҘмқҖ л‘җ к°Җм§Җ мӨ‘ н•ҳлӮҳ лҳҗлҠ” лӘЁл‘җ мҰқк°Җн• л•Ң л°ңмғқн•ңлӢӨ.

м—¬кё°м—җм„ң вҖҳл…ёлҸҷмӢңк°„вҖҷмқҖ к°Ғ л…ёлҸҷмһҗл“Өмқҙ к·јл¬ҙн•ң мӢңк°„кіј л…ёлҸҷмһҗ мҲҳлЎң кі„мғҒлҗңлӢӨ.

вҖҳмӢңк°„лӢ№ мғқмӮ°м„ұвҖҷмқҖ мқјл°ҳм ҒмңјлЎң кё°м—…мқҙ лҚ” л§ҺмқҖ мһҗліё мһҘ비, лҚ” лҶ’мқҖ мҲҳмӨҖмқҳ м—ӯлҹү лҳҗлҠ” мҡ°мҲҳн•ң кё°мҲ мқ„ 추к°Җн• л•Ң мҰқк°Җн•ңлӢӨ.

к·ёл ҮлӢӨл©ҙ лҜёкөӯмқҖ нҳ„мһ¬ м–ҙл– н• к№Ң?

кІҪм ң м„ұмһҘм—җ мҳҒн–Ҙмқ„ лҜём№ҳлҠ” мІ« лІҲм§ё мҡ”мқёмқ„ ліҙмһҗ. л°”лЎң мқёкө¬ мҰқк°Җ л‘”нҷ”мҷҖ лӮ®мқҖ л…ёлҸҷ м°ём—¬мңЁмқҙлӢӨ.

лҜёкөӯм—җм„ң мқёкө¬ мҰқк°Җ л‘”нҷ”лҠ” мқҙлҜј мһҘлІҪкіј лӮ®мқҖ м¶ңмӮ°мңЁлЎң мқён•ҙ л°ңмғқн–ҲлӢӨ. н•ҳм§Җл§Ң л…ёлҸҷ м°ём—¬м—җ л¶Җм •м Ғ мҳҒн–Ҙмқ„ лҒјм№ мҲҳ мһҲлҠ” вҖҳмӮ¬нҡҢ м•Ҳм „л§қвҖҷмңјлЎң мқён•ҙ мғҒнҷ©мқҖ лҚ”мҡұ м•…нҷ”лҗҳм—ҲлӢӨ.

л‘җ лІҲм§ёмқҙмһҗ лҚ” мӢ¬к°Ғн•ң л¬ём ңлҠ” м–јм–ҙл¶ҷмқҖ мғқмӮ°м„ұ мҰқлҢҖм—җ мһҲлӢӨ.

мһҗліё нҲ¬мһҗмҷҖ кё°мҲ л°ңм „мқҖ мқјл°ҳм ҒмңјлЎң к·јл¬ҙ мӢңк°„лӢ№ мғқмӮ°лҹүмқ„ лҶ’м—¬ мӨҖлӢӨ. к·ёлҹ¬лӮҳ лӢ·м»ҙ л¶җ мӢңкё°лҘј м ңмҷён•ҳкі 1973л…„ мқҙнӣ„ мқҙ мҶҚлҸ„к°Җ лҲҲм—җ лқ„кІҢ л‘”нҷ”лҗҳм—ҲлӢӨ.

мҷң мқҙлҹ° мқјмқҙ мқјм–ҙлӮ¬мқ„к№Ң? кІҪм ң л°ңм „мқҙлһҖ мЈјлЎң кё°мҲ л°ңм „м—җ мқҳн•ҙ кІ°м •лҗҳкё° л•Ңл¬ёмқҙлӢӨ.

м ң2м°Ё м„ёкі„лҢҖм „л¶Җн„° 1973л…„ мӮ¬мқҙм—җ мқјм–ҙлӮң мқјмқ„ ліҙмһҗ. лӢ№мӢң мҡ°лҰ¬лҠ” м—„мІӯлӮң мғқмӮ°м„ұ мҰқлҢҖлҘј лӘ©лҸ„н–ҲлҠ”лҚ°, мқҙ мӢңлҢҖлҠ” лҢҖлҹү мғқмӮ°мңјлЎң лҢҖліҖлҗҳлҠ” м„ұмһҘмқҳ нҷ©кёҲкё°мҳҖлӢӨ.

мқҙлҹ¬н•ң мғқмӮ°м„ұмқҳ лҶҖлқјмҡҙ мҰқлҢҖлҠ” м „нӣ„ мӢңмһҘ кё°нҡҢмҷҖ м „мҹҒ мӨ‘ мқҙлЈЁм–ҙ진 мһҗліё нҲ¬мһҗ л°Ҹ мӢ кё°мҲ мқҳ мғҒм—…нҷ”м—җ мқҳн•ҙ к°ҖлҠҘн•ҙмЎҢлӢӨ.

м—¬кё°м—җ мЈјк°„(Interstate) кі мҶҚлҸ„лЎң, н•ӯкіө, TV л°©мҶЎ, н• мқё мҶҢл§Өм җ, лҢҖк·ңлӘЁ мЎ°лҰҪ лқјмқёмқҙ кІ°н•©лҗҳм–ҙ нҷңкё°м°¬ мғқнғңкі„лҘј м§Җмӣҗн–ҲлӢӨ.

н•ҳм§Җл§Ң нҒ¬кІҢ м—јл Өн• н•„мҡ”лҠ” м—ҶлӢӨ. нҳ„мһ¬ мқҙлҹ¬н•ң лҘҳмқҳ нҷ©кёҲкё°к°Җ л””м§Җн„ё кё°мҲ мқҳ л°ңлӢ¬лЎң мһ¬л“ұмһҘн•ҳкі мһҲкё° л•Ңл¬ёмқҙлӢӨ.

мқҙ мғҲлЎңмҡҙ нҷ©кёҲкё°лҠ” 2030л…„лҢҖ мӨ‘л°ҳк№Ңм§Җ м§ҖмҶҚлҗ кІғмңјлЎң мҳҲмғҒлҗңлӢӨ. ліҖнҷ” мӨ‘ лҢҖл¶Җ분мқҖ мһҗм—°мҠӨлҹҪкІҢ л°ңмғқн• кІғмқҙлӢӨ.

лҳҗ лӢӨлҘё ліҖнҷ”л“ӨмқҖ м •л¶Җмқҳ мһҘл ӨлЎңлҸ„ л°ңмғқн• кІғмқҙлӢӨ. л”°лқјм„ң м№ңм„ұмһҘ м •мұ…мқҙ л¬ҙмІҷ мӨ‘мҡ”н•ҳлӢӨ.

кІҪм ң м„ұмһҘ л‘”нҷ”мқҳ м„ё лІҲм§ё мқҙмң лҠ” м§ҖлӮң 15л…„ лҸҷм•Ҳ лҜёкөӯ кІҪм ңлҘј м§Җл°°н•ң мғҒн’Ҳкіј м„ң비мҠӨмқҳ мў…лҘҳлҘј м •лҹүнҷ”н•ҳкё° м–ҙл өлӢӨлҠ” лҚ° мһҲлӢӨ.

к·ё к°Җм№ҳмқҳ лҢҖл¶Җ분мқҙ м§Ҳм Ғмқҙкі мЈјкҙҖм Ғмқҙкё° л•Ңл¬ёмқҙлӢӨ.

мҳҲлҘј л“Өм–ҙ, мҠӨл§ҲнҠёнҸ°мқҖ мң м„ м „нҷ”, GPS мһҘм№ҳ, н…”л Ҳл№„м „, 축мқҢкё°, кі„мӮ°кё°, к°ңмқёмҡ© м»ҙн“Ён„°, мұ…, мӢ л¬ё, мһЎм§Җ л°Ҹ кё°нғҖ мҲҳл§ҺмқҖ мһҘм№ҳлҘј лҢҖмІҙн•ҳм—¬ мҡ°лҰ¬ мӮ¶мқҳ м§Ҳмқ„ н—Өм•„лҰҙ мҲҳ м—Ҷмқ„ м •лҸ„лЎң н–ҘмғҒмӢңмј°лӢӨ.

лҳҗн•ң мҶҢм…ң лҜёл””м–ҙ л°Ҹ м „мһҗмғҒкұ°лһҳ н”Ңлһ«нҸјкіј к°ҷмқҖ мҷ„м „нһҲ мғҲлЎңмҡҙ к°Җм№ҳ мһҗмӮ°мқ„ нҷңм„ұнҷ”н–ҲлӢӨ.

к·ёлҹ¬лӮҳ мқҙлҹ¬н•ң мӢ м ңн’ҲмқҖ лҢҖмІҙ м ңн’Ҳкіј лҸҷмқјн•ң л°©мӢқмңјлЎң GDPм—җ 추к°Җлҗҳм§ҖлҠ” м•ҠлҠ”лӢӨ.

л°Җл ҲлӢҲм–ј мқҙнӣ„мқҳ нҳҒмӢ мқҙ мқҙм „мқҳ л¬јлҰ¬м Ғ м ңн’ҲмқҙлӮҳ мң лЈҢ м„ң비мҠӨлҘј вҖҳл¬ҙлЈҢвҖҷмқё кІғмІҳлҹј ліҙмқҙлҠ” кҙ‘кі м§Җмӣҗ л””м§Җн„ё м„ң비мҠӨлЎң ліҖнҷ”мӢңмј°кё° л•Ңл¬ёмқҙлӢӨ. к·ёлҰ¬кі мқҙлҠ” мў…мў… GDPм—җ л°ҳмҳҒлҗҳм§Җ м•ҠлҠ”лӢӨ.

н•ҳм§Җл§Ң мқҙм ң лҜёкөӯмқҖ вҖҳм§Ҳм Ғ л¬ҙнҳ•мһҗмӮ°вҖҷмқҳ м„ұмһҘм—җм„ң лІ—м–ҙлӮҳ мўҖ лҚ” вҖҳм •лҹүнҷ” к°ҖлҠҘн•ң к°Җм№ҳвҖҷлЎң лҸҢм•„к°ҖлҠ” м „нҷҳмқҳ л¬ён„ұм—җ мһҲлҠ” кІғмңјлЎң ліҙмқёлӢӨ.

мқёкіөм§ҖлҠҘмқҙ м§Җмӣҗн•ҳлҠ” мӢ м•Ҫ, мһ¬лЈҢ, кё°кі„, н”„лЎңм„ёмҠӨ л°Ҹ м„ң비мҠӨк°Җ мӢӨм ңлЎң GDPм—җ лӮҳнғҖлӮҳлҠ” мғҲлЎңмҡҙ мғқмӮ° мҲҳмқөлҝҗл§Ң м•„лӢҲлқј м—°кі„ л°Ҹ мң кҙҖ мҲҳмқөмқ„ м°Ҫм¶ңн• кІғмқҙкё° л•Ңл¬ёмқҙлӢӨ.

лӢӨмқҢмқҖ вҖңмҶҢл“қ л¶ҲнҸүл“ұмқҙ лҶҖлқјмҡҙ мҶҚлҸ„лЎң кі„мҶҚ кі мЎ°лҗҳкі мһҲлӢӨвҖқлҠ” мЈјмһҘмқ„ мӮҙнҺҙліҙмһҗ.

лҜё мқҳнҡҢ мҳҲмӮ°мІҳлҠ” кі мҶҢл“қ к°Җкө¬мҷҖ м ҖмҶҢл“қ к°Җкө¬ к°„мқҳ мҶҢл“қ кІ©м°ЁлҘј м¶”м •н•ҳкё° мң„н•ҙ м§ҖлӢҲкі„мҲҳлҘј мӮ¬мҡ©н•ңлӢӨ.

мқҙлҹ¬н•ң кі„мӮ°м—җлҠ” мқјл°ҳм ҒмңјлЎң л‘җ к°Җм§Җ мёЎм • л°©лІ•мқҙ мӮ¬мҡ©лҗҳлҠ”лҚ°, мһ¬лҜёмһҲлҠ” кІғмқҖ л¶ҲнҸүл“ұ 추세м—җ лҢҖн•ҙ м„ңлЎң лӢӨлҘё лӢөмқ„ м ңкіөн•ңлӢӨлҠ” м җмқҙлӢӨ.

мёЎм • л°©лІ• мӨ‘ н•ҳлӮҳлҠ” мҶҢмң„ м„ём „ мҶҢл“қмқ„ кё°мӨҖмңјлЎң н•ң вҖҳмӢңмһҘ мҶҢл“қвҖҷмқҙкі , лӢӨлҘё н•ҳлӮҳлҠ” вҖҳм„ёнӣ„ л°Ҹ м–‘лҸ„ мҶҢл“қвҖҷмқҙлӢӨ.

л¶ҲнҸүл“ұмқ„ мёЎм •н•ҳлҠ” лҚ° мһҲм–ҙ м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қмқҖ мқҳлҜёк°Җ мһҲлҠ” мң мқјн•ң м§Җн‘ңмқҙлӢӨ.

мӢңмһҘ мҶҢл“қкіј лӢ¬лҰ¬, м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қмқҖ мғқнҷңмҲҳмӨҖм—җ лҢҖн•ң мў…н•©м Ғмқё мёЎм •м№ҳмқҙкё° л•Ңл¬ёмқҙлӢӨ.

мҰү, көӯлҜјмқҳ мӢӨм ң кІҪм ңм Ғ нӣ„мғқм—җ лҜём№ҳлҠ” м„ёкёҲкіј мӮ¬нҡҢм Ғ м•Ҳм •л§қмқҳ мҳҒн–Ҙл Ҙмқ„ кі л Өн•ң кІғмқҙлӢӨ.

м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қ кё°мӨҖмқ„ кё°л°ҳмңјлЎң, л¶ҲнҸүл“ұмқҖ 1990л…„л¶Җн„° 2019л…„к№Ңм§Җ 30л…„ лҸҷм•Ҳ 7% мҰқк°Җн–ҲлӢӨ. к·ёлҹ¬лӮҳ м „мІҙ мҰқк°ҖлҠ” 1990л…„л¶Җн„° 2007л…„м—җ 집мӨ‘м ҒмңјлЎң лӮҳнғҖлӮ¬лӢӨ.

л°ҳл©ҙ, мқҙлҹ¬н•ң л¶ҲнҸүл“ұмқҙ 2007л…„ мқҙнӣ„м—җлҠ” 5% к°җмҶҢн•ң кІғмңјлЎң лӮҳнғҖлӮ¬лӢӨ.

л¶ҲнҸүл“ұмқҖ кёҲмңө мң„кё°мҷҖ мӣ”мҠӨнҠёлҰ¬нҠё м җл № мӢңмң„лЎң мөңкі мЎ°м—җ лӢ¬н–Ҳм§Җл§Ң, м •лҰ¬н•ҳмһҗл©ҙ лҜёкөӯмқҳ мҶҢл“қ л¶ҲнҸүл“ұмқҖ мӢӨм ңлЎң м§ҖлӮң 16л…„ лҸҷм•Ҳ мӨ„м–ҙл“Өм—ҲлӢӨ.

лӢӨмқҢмқҖ вҖңл¶Җмұ„ мҲҳмӨҖмқҙ кҙҖлҰ¬н•ҳкё° м–ҙл Өмҡё м§ҖкІҪм—җ мқҙлҘҙл ҖлӢӨвҖқлҘј мӮҙнҺҙліҙмһҗ.

мЈјмһҘмқҳ н•өмӢ¬мқҖ мқҙкІғмқҙ м•һмңјлЎң мҲҳл…„ лӮҙм—җ м№ҳлӘ…м Ғмқё л¬ём ңлҘј м•јкё°н• кІғмқҙлқјлҠ” м җмқҙлӢӨ.

мқҙкІғмқҙ мӮ¬мӢӨмқјк№Ң? лЁјм Җ лҜёкөӯмқҳ к°Җкі„ лҢҖм°ЁлҢҖмЎ°н‘ң мғҒнғңлҘј мӮҙнҺҙліҙл©ҙ, нҳ„мһ¬ лҜјк°„ л¶Җл¬ё мҲңмһҗмӮ°мқҖ 154мЎ° 3мІңм–ө лӢ¬лҹ¬лЎң 10л…„ м „мқҳ кұ°мқҳ л‘җ л°°м—җ лӢ¬н•ңлӢӨ.

мқён”Ңл Ҳмқҙм…ҳ мЎ°м • мқҙнӣ„ лҜёкөӯ к°Җкө¬мқҳ мҲңмһҗмӮ°мқҖ 1952л…„ мқҙнӣ„ л§Өл…„ нҸүк· 3.6% мҰқк°Җн•ҙ мҷ”кі , мқҙлҠ” 70л…„ л§Ңм—җ 12л°° мҰқк°Җн•ң мҲҳм№ҳмқҙлӢӨ.

к°ҷмқҖ кё°к°„ мқёкө¬лҸ„ л§Һмқҙ лҠҳм—ҲлӢӨлҠ” нҸүмқҙ мһҲм§Җл§Ң, мқён”Ңл Ҳмқҙм…ҳ мЎ°м • мқҙнӣ„ 1мқёлӢ№ лҚ°мқҙн„°лҘј мӮҙнҺҙліҙл©ҙ нҸүк· лҜёкөӯмқёмқҳ мғқнҷңмҲҳмӨҖмқҙ м§ҖлӮң 73л…„ лҸҷм•Ҳ кұ°мқҳ 6л°°лӮҳ лҶ’м•„мЎҢлӢӨлҠ” кІғмқ„ м•Ң мҲҳ мһҲлӢӨ.

GDP лҢҖ비 м—°л°© л¶Җмұ„к°Җ лҢҖлһө 124%лқјлҠ” кІғмқҖ мғқк°Ғн•ҙліј м—¬м§Җк°Җ мһҲлҠ” мҲҳм№ҳмқҙлӢӨ.

м „нӣ„ кұ°лҢҖн•ң л¶җмқҙ мӢңмһ‘лҗҳл ӨлҚҳ 2м°Ё м„ёкі„лҢҖм „ л§җ, мқҙ мҲҳм№ҳк°Җ 119%к№Ңм§Җ м№ҳмҶҹм•ҳлӢӨлҠ” м җм—җ мЈјлӘ©н•ҳмһҗ.

мқҙнӣ„ 1970л…„лҢҖ мӨ‘л°ҳм—җлҠ” м•Ҫ 32%лЎң мөңм Җ мҲҳмӨҖмңјлЎң л–Ём–ҙмЎҢкі 2001л…„м—җлҠ” 55%лҘј мЎ°кёҲ л„ҳлҠ” мҲҳмӨҖмңјлЎң мғҒмҠ№н–ҲлӢӨ.

нҳ„мһ¬мқҳ мҲҳм№ҳлҠ” кёҲмңө мң„кё° л°Ҹ мҪ”лЎңлӮҳ19 лҢҖмң н–үкіј кҙҖл Ёлҗң л¶Җм–‘мұ…мқҳ м—¬нҢҢлЎң л°ңмғқн•ң кІғмқҙлӢӨ.

124%лҠ” лҶ’лӢӨкі ліј мҲҳ мһҲм§Җл§Ң, м—°л°©мӨҖ비мқҖн–үмқҙ кёҲлҰ¬лҘј нҶөн•ҙ м •л¶Җмқҳ л¶Җмұ„ мғҒнҷҳ л¶ҖлӢҙмқ„ мЎ°м •н•ҳкі мһҲлӢӨ.

лҳҗн•ң лҜёкөӯ мқҙмҷёмқҳ лІ•мқём—җ лҢҖн•ң л¶Җмұ„лҠ” м „мІҙмқҳ 23%м—җ л¶Ҳкіјн•ҳл©°, лҚ” мӨ‘мҡ”н•ң кІғмқҖ л¶Җмұ„к°Җ лҜёкөӯ лӢ¬лҹ¬лЎңл§Ң н‘ңмӢңлҗҳкё° л•Ңл¬ём—җ м—°л°© м •л¶ҖлҠ” лҢҖл¶Җ분мқҳ лӢӨлҘё көӯк°Җк°Җ көӯк°Җ л¶Җмұ„мҷҖ кҙҖл Ён•ҳм—¬ м§Ғл©ҙн•ҳлҠ” л””нҸҙнҠё мң„н—ҳм—җ м§Ғл©ҙн•ҳм§Җ м•ҠлҠ”лӢӨлҠ” м җмқҙлӢӨ.

к·ёлҰ¬кі мҡ°лҰ¬к°Җ мЈјлӘ©н•ҙм•ј н• кІғмқҖ лҜёкөӯмқҳ кІҪм ңм Ғ, м§Җм •н•ҷм Ғ мқҙм җмқҙ м•һмңјлЎңлҸ„ кі„мҶҚ кёҚм •м ҒмқҙлқјлҠ” лҚ° мһҲлӢӨ.

мқҙлҠ” н–Ҙнӣ„ мҲҳмӢӯ л…„ лҸҷм•Ҳ лҜёкөӯмқҳ GDPк°Җ м •л¶Җ л¶Җмұ„ліҙлӢӨ л№ лҘҙкІҢ мҰқк°Җн•ҳм—¬ мқҙ 비мңЁмқ„ лӮ®м¶ң к°ҖлҠҘм„ұмқҙ нҒ¬лӢӨлҠ” мқҳлҜёмқҙлӢӨ.

л¬јлЎ , м •л¶Җ л¶Җл¬ёмқҙ м•„лӢҢ лҜјк°„ л¶Җл¬ёмқҳ м–ҙлҠҗ мӢңм җм—җм„ң нҢҢмӮ°мқҙлӮҳ мұ„л¬ҙ л¶Ҳмқҙн–ү к°ҖлҠҘм„ұмқҙ м ңлЎңлҠ” м•„лӢҗ кІғмқҙлӢӨ.

лӢӨл§Ң 2007л…„ мқҙнӣ„ лҜјк°„ л¶Җл¬ёмқҳ л¶Җмұ„к°Җ м•Ҫ 40% к°җмҶҢн–Ҳкі , GDP лҢҖ비 лҜјк°„ л¶Җл¬ё л¶Җмұ„ 비мңЁмқҙ мқҙм ң 1970л…„лҢҖ мҙҲ мҲҳмӨҖмңјлЎң лҗҳлҸҢм•„к°”лӢӨ.

мў…н•©м ҒмңјлЎң 분м„қн–Ҳмқ„ л•Ң, лҜёкөӯмқҳ л¶Җмұ„ мҲҳмӨҖмқҖ мҡ°л Өн• мғҒнҷ©мқҖ м•„лӢҲлӢӨ. лӢӨл§Ң лҜёкөӯ м •л¶ҖлҠ” 비мғқмӮ°м Ғмқё мҡ°м„ мҲңмң„м—җ мһҗкёҲмқ„ мЎ°лӢ¬н•ҳкё° мң„н•ң м°Ёмһ…мқ„ м•һмңјлЎңлҸ„ м§Җм–‘н•ҙм•ј н• кІғмқҙлӢӨ.

лӢӨмқҢмңјлЎң вҖңмғқмӮ°м„ұкіј л…ёлҸҷмһҗ мһ„кёҲ к°„ м—°кІ°мқҙ лҒҠм–ҙмЎҢлӢӨвҖқлҠ” мЈјмһҘмқ„ мӮҙнҺҙліҙмһҗ.

мқҙм—җ лҢҖн•ң лӢөмқҖ вҖҳк·ёл Үм§Җ м•ҠлӢӨ!вҖҷмқҙлӢӨ. лҜёкөӯкё°м—…м—°кө¬мҶҢ(American Enterprise Institute) кІҪм ңн•ҷмһҗ л§ҲмқҙнҒҙ R. мҠӨнҠёл Ҳмқё(Michael R. Strain)мқҖ мҳӨнһҲл Ө вҖҳмғқмӮ°м„ұкіј л…ёлҸҷмһҗ мһ„кёҲ мӮ¬мқҙмқҳ м—°кҙҖм„ұмқҙ к°•л Ҙн•ҳлӢӨвҖҷлҠ” мЈјмһҘмқ„ нҺјм№ңлӢӨ.

к·ёлҠ” мғқмӮ°м„ұ мҰқк°ҖмҷҖ л…ёлҸҷмһҗ мһ„кёҲ мҰқк°Җк°Җ 10л…„ лӢЁмң„лЎң н•Ёк»ҳ мӣҖм§ҒмқёлӢӨлҠ” кІғмқ„ 분м„қн–Ҳкі , 2000л…„ мқҙнӣ„ м•Ҫк°„мқҳ м°Ёмқҙл§Ң мһҲмқ„ лҝҗ, лӢЁм Ҳмқҳ мҰқкұ°лҠ” м—ҶлӢӨкі л§җн•ңлӢӨ.

мҠӨнҠёл ҲмқёмқҖ мғқмӮ°лҹүмқ„ мҙқ мғқмӮ°лҹүмқҙ м•„лӢҢ мҲң мғқмӮ°лҹүмңјлЎң м •мқҳн•ңлӢӨ.

мһ‘м—… мӢңк°„лӢ№ мҲң мғқмӮ°лҹүмқ„ кё°мӨҖмңјлЎң кі„мғҒлҗң мғқмӮ°м„ұмқҖ мһҗліё к°җк°ҖмғҒк°Ғмқ„ м ңкұ°н•ҳлҜҖлЎң мқҳлҜёк°Җ мһҲлӢӨ.

вҖҳк°җк°ҖмғҒк°Ғ비вҖҷлҠ” мҶҢл“қмқҳ мӣҗмІңмқҙ м•„лӢҲкё° л•Ңл¬ём—җ л…ёлҸҷмһҗ ліҙмғҒкіј мғқмӮ°м„ұ мӮ¬мқҙмқҳ м—°кҙҖм„ұмқ„ мЎ°мӮ¬н• л•Ң мҲң мғқмӮ°лҹүмқҙ лҚ” лӮҳмқҖ мІҷлҸ„мқҙлӢӨ.

лҳҗ н•ҳлӮҳ кі л Өн•ҙм•ј н• кІғмқҖ 비мһ„кёҲмқҳ 비мӨ‘мқҙлӢӨ.

м „мІҙм Ғмқё л…ёлҸҷмһҗ ліҙмғҒм—җм„ң 비мһ„кёҲмқҙ м°Ём§Җн•ҳлҠ” 비мӨ‘мқҙ лҶ’м•„мЎҢлӢӨлҠ” кІғмқҙ мӮ¬мӢӨмқҙлӢӨ.

л”°лқјм„ң лӢЁмҲңн•ң мһ„кёҲліҙмғҒліҙлӢӨлҠ” кұҙк°•ліҙн—ҳ л“ұ 비мһ„кёҲ ліҙмғҒмқ„ мқҙлҹ¬н•ң кө¬мЎ°м—җ нҸ¬н•ЁмӢңнӮӨлҠ” кІғмқҙ л°”лһҢм§Ғн•ҳлӢӨ.

мқҙлҹ¬н•ң 분м„қ кІ°кіјлҠ” лҜёкөӯм—җм„ң мғқмӮ°м„ұкіј мһ„кёҲ мӮ¬мқҙмқҳ м—°кҙҖм„ұмқҖ м—¬м „нһҲ к°•л Ҙн•ҳлӢӨлҠ” кІғмқ„ 분лӘ…нһҲ ліҙм—¬мӨҖлӢӨ.

кІ°кіјм ҒмңјлЎң, лҜёкөӯмқҳ л…ёлҸҷмһҗл“Өмқҙ мӢңмҠӨн…ңм—җ лҢҖн•ң кё°м—¬лҸ„м—җ 비н•ҙ л¶ҖмЎұн•ң лҢҖмҡ°лҘј л°ӣкі мһҲлӢӨкі мЈјмһҘн• мқҙмң лҠ” кұ°мқҳ м—ҶлӢӨкі н• мҲҳ мһҲлӢӨ.

вҖңл…ёлҸҷмһҗ мһ„кёҲмқҖ мҲҳмӢӯ л…„ лҸҷм•Ҳ м •мІҙлҗҳм—ҲлӢӨвҖқлҠ” мЈјмһҘмқҖ м–ҙл–Ёк№Ң?

мқҙ мЈјмһҘмқҳ к°ҖмһҘ мқјл°ҳм Ғ лІ„м „мқҖ вҖң1970л…„лҢҖ мқҙнӣ„ мӢӨм§Ҳмһ„кёҲмқҙ м „нҳҖ мҳӨлҘҙм§Җ м•Ҡм•ҳмңјл©°, мқҙлҘј к°җм•Ҳн•ҳл©ҙ м§ҖлӮң 50л…„ лҸҷм•Ҳ мһ„кёҲмқҙ лӢЁм§Җ 5%л§Ң мҳ¬лһҗлӢӨвҖқлҠ” кІғмқҙлӢӨ.

мқҙлҹ¬н•ң мЈјмһҘмқҖ мһҘкё°м Ғмқҙкі кҙ‘лІ”мң„н•ң мһ„кёҲ м№ЁмІҙ нҳ№мқҖ м •мІҙлқјлҠ” к°ңл…җмңјлЎң мқҙлҸҷн•ңлӢӨ.

к·ёлҹ¬лӮҳ мӢӨм ңлЎң к·ёлҹҙк№Ң?

1990л…„ кІҪкё° мЈјкё° м •м җл¶Җн„° 2019л…„к№Ңм§Җ мӢӨм§Ҳмһ„кёҲмқҖ мҶҢ비мһҗл¬јк°Җм§ҖмҲҳ лҢҖ비 20%, л¬јк°ҖмҶҢ비м§Җм¶ң(PCE) лҢҖ비 33% мқҙмғҒ мғҒмҠ№н–ҲлӢӨ.

мҠӨнҠёл Ҳмқёмқҙ к°•мЎ°н•ҳлҠ” м§Җн‘ңлҘј кі„мғҒн–Ҳмқ„ л•ҢлҠ” мқҙл ҮкІҢ лӢӨлҘё м§ҖмҲҳк°Җ л“ұмһҘн•ңлӢӨ.

лҚ”мҡұмқҙ, м„ёнӣ„ мҲҳмқөкіј м–‘лҸ„ мҲҳмқөмқ„ кё°мӨҖмңјлЎң мӮ¬лһҢл“Өмқҙ м–јл§ҲлӮҳ л§ҺмқҖ лҸҲмқ„ к°Җм§Җкі мһҲлҠ”м§Җ кі л Өн•ңлӢӨл©ҙ м№ЁмІҙлҘј мЈјмһҘн•ҳкё°лҠ” м–ҙл өлӢӨ.

лҜё мқҳнҡҢ мҳҲмӮ°мІҳк°Җ 1979л…„л¶Җн„° 2019л…„к№Ңм§Җ мҶҢл“қмқ„ мөңк·ј мЎ°мӮ¬н•ң кІ°кіј лӢӨмқҢкіј к°ҷмқҖ 5к°Җм§Җ мӮ¬мӢӨмқҙ нҷ•мқёлҗҳм—ҲлӢӨ.

мІ«м§ё, 2019л…„ кё°мӨҖ лӘЁл“ мҶҢл“қ к·ёлЈ№мқҖ нҸүк· м ҒмңјлЎң к°ҖмһҘ лҶ’мқҖ м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қмқ„ кё°лЎқн–ҲлӢӨ.

л‘ҳм§ё, м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қ мҰқк°Җк°Җ мғҒмң„ к°Җкө¬м—җм„ң к°ҖмһҘ л№ лҘҙкІҢ л°ңмғқн–Ҳм§Җл§Ң, лҲ„진세мҷҖ мӮ¬нҡҢ м•Ҳм „л§қ к°•нҷ”лЎң мқён•ҙ м „ к°Җкө¬мқҳ мҰқк°Җ мҲҳмӨҖмқҖ нҸүк· мқ„ мқҙлӨҳлӢӨ.

м…Ӣм§ё, м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қм—җ лҢҖн•ң мөңн•ҳмң„ 5분мң„ мҶҢл“қмқҖ м „мІҙм ҒмңјлЎң 94% мҰқк°Җ, м—°к°„ 1.7%м”© мҰқк°Җн–ҲлӢӨ.

л„·м§ё, м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қм—җ лҢҖн•ң мӨ‘мң„ 3분мң„ мҶҢл“қмқҖ м „мІҙм ҒмңјлЎң 59% мҰқк°Җ, м—°к°„ 1.2%м”© мҰқк°Җн–ҲлӢӨ.

лӢӨм„Ҝм§ё, м„ёнӣ„ мҶҢл“қкіј м–‘лҸ„ мҶҢл“қм—җ лҢҖн•ң мөңкі 5분мң„ мҶҢл“қмқҖ 123% мҰқк°Җ, м—°к°„ 2.0%м”© мҰқк°Җн•ҳм—¬ 1979л…„ 113,100лӢ¬лҹ¬м—җм„ң 2019л…„м—җлҠ” 252,100лӢ¬лҹ¬м—җ мқҙлҘҙл ҖлӢӨ.

мөңкі мҶҢл“қ к°Җкө¬мқҳ мҶҢл“қ мҰқк°Җк°Җ м•Ҫк°„ лҚ” л№ лҘё мқҙмң лҠ” нҸүк· м—°л°© м„ёмңЁмқҙ к°җмҶҢн•ҳмҳҖкё° л•Ңл¬ёмқҙлӢӨ.

м „мІҙм ҒмңјлЎң, лҜёкөӯм—җм„ң м „ к°Җкө¬мқҳ мҶҢл“қмқҖ мҡ°мғҒн–Ҙ мқҙлҸҷн•ҳкі мһҲлӢӨ.

кі„мёө к°„мқҳ мҶҢл“қ 분нҸ¬л§Ң кі л Өн•ҙлҸ„ мқҙкІғмқҖ мӮ¬мӢӨмқёлҚ°, 40лҢҖ лҜёкөӯмқёмқҳ м•Ҫ 73%к°Җ л¶ҖлӘЁ м„ёлҢҖліҙлӢӨ мӢӨм§Ҳ мҶҢл“қмқҙ лҚ” лҶ’мқҖ кІғмңјлЎң лӮҳнғҖлӮ¬лӢӨ.

кІ°лЎ мқҖ л¬ҙм—Үмқёк°Җ? лҜёкөӯ кІҪм ңк°Җ кіјмҶҢнҸүк°Җлҗҳкі мҳӨн•ҙлҘј л°ӣкі мһҲлӢӨлҠ” кІғмқҙлӢӨ.

лҳҗн•ң лҜёлһҳм—җ лҢҖн•ң мҡ°л ӨмҷҖ лӢ¬лҰ¬, мӢӨм§Ҳм Ғ лҜёкөӯ кІҪм ңлҘј ліҙл©ҙ лҜёлһҳк°Җ л¶Җм •м Ғмқј мқҙмң к°Җ м—ҶлӢӨлҠ” кІғмқҙлӢӨ.

мқҙлҹ¬н•ң 추세лҘј кі л Өн•ҳм—¬ мҡ°лҰ¬лҠ” лӢӨмқҢкіј к°ҷмқҖ мҳҲмёЎмқ„ лӮҙлҰ°лӢӨ.

мІ«м§ё, н–Ҙнӣ„ 10л…„ лҸҷм•Ҳ мӢӨм§Ҳм Ғмқё лҜёкөӯмқҳ кІҪм ңм„ұмһҘлҘ мқҖ кёҲмңөмң„кё° мқҙм „мқё 3.1% 추세лЎң лҗҳлҸҢм•„к°Ҳ кІғмқҙлӢӨ.

мқҙлҹ¬н•ң м„ұмһҘмқҳ л°°кІҪм—җлҠ” м„ёкі„ мөңкі мҲҳмӨҖмқҳ м••лҸ„м Ғмқё мқёкіөм§ҖлҠҘ кё°мҲ кіј л°ңм „, мқҙлҘј нҶөн•ң мғқмӮ°м„ұмқҳ нҖҖн…Җ м җн”„, лӢӨм–‘н•ң мқ‘мҡ©кіј м Ғмҡ©, м„ёкі„ мөңкі мқҳ мқёмһ¬ ліҙмң к°Җ мһҲлӢӨ.

л‘ҳм§ё, лҜёкөӯмқҳ кІҪм ң м„ұмһҘкіј л¶Җнҷңмқҳ к°ҖмһҘ нҒ° мң„нҳ‘мқҖ мҷёл¶Җк°Җ м•„лӢҢ лӮҙл¶Җ, мҰү м§ҖмҶҚм Ғмқё кіјмһү к·ңм ңмҷҖ кҙҖл Ёмқҙ мһҲмқ„ кІғмқҙлӢӨ.

мҳҲм „ кё°мӨҖм—җ мқҳн•ҙ нғ„мғқн–Ҳм§Җл§Ң нҳ„мһ¬ кё°мӨҖм—җлҠ” л§һм§Җ м•ҠлҠ”, 비мғқмӮ°м Ғмқё к·ңм •л“Ө, к·ёлҰ¬кі мқҙ к·ңм •мқ„ мӨҖмҲҳн•ҳлҠ” лҚ° л“ңлҠ” мҳҲмӮ°кіј мһҗмӣҗ лӮӯ비к°Җ мҡ°м„ мһ¬нҺёлҗҳм–ҙм•ј н• кІғмқҙлӢӨ.

лҜёкөӯ кІҪм ңм—җ м§ҖлӮң 40л…„ лҸҷм•Ҳ лҲ„м Ғлҗң мһҳлӘ»лҗң к·ңм •л“Өмқҙ л№ лҘҙкІҢ м ңкұ°лҗҳм–ҙм•јл§Ң GDP м„ұмһҘлҘ мқ„ м—°к°„ мөңмҶҢ 1%м”© лҚ” мҳҒкө¬м ҒмңјлЎң лҶ’мқј мҲҳ мһҲлӢӨ.

м…Ӣм§ё, 2020л…„лҢҖ лҜёкөӯмқҳ м„ұмһҘмқҖ м „ м„ёкі„м Ғмқё мқёкө¬нҶөкі„н•ҷм Ғ мң„кё°лЎң мқён•ҙ лҚ”мҡұ лҚ” нҒ° мқҙмқөмқ„ л°ңмғқмӢңнӮ¬ кІғмқҙлӢӨ.

мӨ‘көӯмңјлЎң лҢҖліҖлҗҳлҠ” мғҲлЎңмҡҙ лғүм „мқҖ мһҗмӣҗкіј кё°мҲ мқҳ м „ м„ёкі„м Ғ нқҗлҰ„мқ„ м җм җ лҚ” м ңн•ңн• кІғмқҙлӢӨ. мқҙлЎң мқён•ң мӢӨм§Ҳм Ғ н”јн•ҙлҠ” мӨ‘көӯкіј лҹ¬мӢңм•„мқҳ кІҪм ң лҸҷ맹мқҙлӢӨ.

мқёкө¬нҶөкі„н•ҷм Ғ нҳ„мӢӨлҸ„ лҜёкөӯм—җкІҢ мң лҰ¬н•ҳлӢӨ. нҳ„лҢҖ лҢҖл¶Җ분мқҳ мң лҹҪкіј м•„мӢңм•„ көӯк°Җл“Өмқҳ мқёл ҘмқҖ кёүмҶҚнһҲ л…ёл №нҷ”, 축мҶҢнҷ”лҗҳм–ҙ кІҪм ң м„ұмһҘ к°ҖлҠҘм„ұмқ„ м ңн•ңн•ҳкі мһҲлӢӨ.

мқҙ л‘җ к°Җм§Җ мқҙмң лЎң лҜёкөӯмқҳ лҰ¬мҮјм–ҙл§Ғкіј лҸҷ맹көӯл“Өмқҳ мҮјм–ҙл§Ғмқҙ к°ҖмҶҚнҷ”лҗҳл©ҙм„ң, к°ҖмһҘ мҡ°мҲҳн•ҳкі лӣ°м–ҙлӮң мқёл Ҙл“Өмқҙ к°ҖмһҘ нҒ¬кІҢ м„ұмһҘн• мҲҳ мһҲлҠ” кіімңјлЎң мқҙлҸҷн•ҳкІҢ лҗ кІғмқҙлӢӨ.

м—¬лҹ¬ м§Җм—ӯмқҙ л¬јл§қм—җ мҳӨлҘј мҲҳ мһҲм§Җл§Ң нҳ„мһ¬лЎңм„ңлҠ” лҜёкөӯмқҙ к·ёмӨ‘ к°ҖмһҘ л§Өл Ҙм Ғмқё кіімһ„мқҖ 분лӘ…н•ҳлӢӨ.

л„·м§ё, к°ңмқёмқҳ нҠ№м • кё°мҲ л Ҙкіј м—ӯлҹүм—җ н”„лҰ¬лҜём—„мқҙ нҒ¬кІҢ л¶Җкіјлҗҳл©ҙм„ң, м ҲлҢҖм Ғмқё мҶҢл“қ л¶ҲнҸүл“ұмқҙ мҶҢнҸӯ мҰқк°Җн• к°ҖлҠҘм„ұмқҙ лҶ’лӢӨ.

мқҙлҹ¬н•ң мҰқк°ҖлҠ” мҲҷл Ёлҗң лё”лЈЁм№јлқј л…ёлҸҷл Ҙмқҙ л¶ҖмЎұн•ң кіім—җм„ң лҚ”мҡұ нҒ¬кІҢ л¶Җк°Ғлҗ кІғмқҙлӢӨ.

лӢӨм„Ҝм§ё, мқёкіөм§ҖлҠҘмқ„ нҶөн•ң мғқмӮ°м„ұ мҰқлҢҖк°Җ мӢңмһ‘лҗҳл©ҙм„ң GDP лҢҖ비 көӯк°Җ л¶Җмұ„ 비мңЁмқҖ мӨ„м–ҙл“Ө кІғмқҙлӢӨ.

GDPмқҳ л№ лҘё м„ұмһҘмқҖ м„ёмһ…мқ„ мҰқк°ҖмӢңмјң л¶Җмұ„ 비мңЁмқ„ л–Ём–ҙлңЁлҰҙ кІғмқҙлӢӨ.

1990л…„лҢҖмҷҖ л§Ҳм°¬к°Җм§ҖлЎң, кё°мҲ мӨ‘мӢ¬мқҳ кІҪм ң л¶җмқҖ лҚ” л§ҺмқҖ нқ‘мһҗлҘј м°Ҫм¶ңн•ңлӢӨ.

лӮ®мқҖ мқҙмһҗмңЁкіј кІ°н•©н•ҳм—¬ мқҙлҹ¬н•ң мҡ”мҶҢл“Өмқҙ көӯк°Җ л¶Җмұ„ 비мңЁмқ„ лӮ®м¶”кІҢ лҗ кІғмқҙлӢӨ.

м—¬м„Ҝм§ё, лҢҖл¶Җ분мқҳ мӮ°м—…м—җм„ң мқҙмңӨнҸӯмқҙ нҷ•лҢҖлҗҳл©ҙм„ң, м „мІҙ л…ёлҸҷмһҗ ліҙмғҒмқҙ кі„мҶҚн•ҙм„ң мғқмӮ°м„ұкіј ліҙмЎ°лҘј л§һм¶ң кІғмқҙлӢӨ.

лҳҗн•ң мқҙмқөм—җ лҢҖн•ң кё°мҲ мқҳ кё°м—¬лҸ„к°Җ лҶ’м•„м§җм—җ л”°лқј мЈјмЈј мҲҳмқөлҸ„ к°ҖмҶҚнҷ”лҗ кІғмқҙлӢӨ.

мқҙлҹ¬н•ң мқҙмқөмқҖ л…ёлҸҷмһҗ нқ¬мғқмқ„ кё°л°ҳмңјлЎң л°ңмғқн•ҳм§ҖлҠ” м•Ҡмқ„ кІғмқҙлӢӨ.

Resource List

1. Faster, Please! September 4, 2023. JAMES PETHOKOUKIS. What is the outlook for long-term US economic growth?

2. Seeking Alpha. August 30, 2023. Scott Grannis. Is This A Great Country Or What?

3. Seeking Alpha. August 30, 2023. Scott Grannis. 2% Growth And 2% Inflation: The FedвҖҷs Done.

4. Faster, Please! August 21, 2023. JAMES PETHOKOUKIS. Four shocking truths about the American economy! (Well, shocking to some.)

5. Trends. October 11, 2014. Trends Editors. AmericaвҖҷs Slow, Painful Techno-Economic Transition.

AmericaвҖҷs Mis-underestimated Economic Reality

By Global Trends Editor Group

Unless youвҖҷve turned off your access to television or the World Wide Web, youвҖҷve certainly heard pundits and politicians making the following six provocative assertions about the U.S. economy:

1. Economic growth has slowed to unacceptable levels;

2. Income inequality continues to rise at an alarming rate;

3. Debt levels are unmanageable;

4. The link between productivity and worker pay is broken;

5. Worker wages have gone nowhere for decades; and

6. Upward mobility is a thing of the past.

In reality, each of these assertions is demonstrably false!

However, there are related trends which, if left unaddressed, could diminish some of AmericaвҖҷs core competitive advantages in the years ahead.

Given the growing gap between perception and reality, letвҖҷs examine these beliefs and why they are so prevalent.

LetвҖҷs start with the assertion that, вҖңEconomic growth has slowed to unacceptable levels.вҖқ

In this case the perception is partially correct.

Since the beginning of the Great Financial Crisis, the growth trend-line for real U.S GDP has slowed from a long-term rate of 3.1% a year to just 2.1% a year.

And while this is historically lackluster, it has enabled the U.S. economy to grow 82% over the past 15 years, while Europe has grown just 6%!

AmericaвҖҷs downshift in growth was caused by three factors which are easy to understand.

Output is defined by вҖңhours workedвҖқ times вҖңproductivity per hour.вҖқ

Growth arises when either or both of those numbers grows.

вҖңHours workedвҖқ is constrained by the number of hours worked by each worker and the number of workers.

Productivity-per-hour typically grows when businesses add more capital equipment, higher levels of skill, or superior technologies.

The first factor impacting U.S. economic growth is slowing population growth coupled with lower labor force participation rates.

This slowdown in population growth is caused by immigration barriers combined with low birth rates.

However, itвҖҷs exacerbated by a social safety net which fails to demand workforce participation.

If we examine real GDP per capita, we see that going all the way back to the Civil War, real per capita growth has varied only modestly from an average of 2% a year, compounded.

That confirms that demography places real limits on what is possible.

A second and more serious problem is glacial productivity growth.

Capital investments and increased skills typically raise output per hour worked.

However, the rate slowed markedly after 1973, except during the Dot-Com boom.

Why? Because economic progress is determined largely by technological progress.

As weвҖҷve explained in prior issues, the enormous surge in productivity we saw between World War II and 1973 represented the вҖңgolden ageвҖқ of the Mass Production Era.

That extraordinary surge in productivity was enabled by post-war market opportunities coupled with commercialization of the capital investments and discoveries made during the war.

Interstate highways, airlines, broadcast TV, discount retailers, and large-scale assembly lines combined to support a vibrant ecosystem.

As highlighted in trend #2 this month, digital technology is now in a similar golden age which is forecasted to run through the mid-2030s.

Many of these changes will happen naturally, but others will need to be encouraged.

Important pro-growth policy adjustments are addressed in trend #3.

The third reason for this down-shift in economic growth is that the kinds of goods and services dominating the U.S. economy over the past 15 years are difficult to quantify.

ThatвҖҷs because most of their value is qualitative and subjective. For example, smart phones have added immeasurably to our quality of life by replacing landline phones,

GPS devices, televisions, phonographs, calculators, personal computers, books, newspapers, magazines and myriad other devices.

TheyвҖҷve also enabled whole new sources of value like social media and e-commerce platforms.

However, these new products donвҖҷt add to GDP in the same way as the products they replaced.

ThatвҖҷs because post-millennial innovation has transformed what were formerly physical products or paid services into ad-supported digital services which appear to be вҖңfree.вҖқ

And these often donвҖҷt show up in GDP.

However, it appears that America is on the verge of a transition away from growth in вҖңqualitative intangiblesвҖқ and back to more вҖңquantifiable value.вҖқ

ThatвҖҷs because the new drugs, materials, machines, processes and services enabled by AI will drive new production and related revenues which actually show up in GDP.

Now, letвҖҷs examine the claim that U.S. вҖңincome inequality continues to rise at an alarming rate.вҖқ

The Congressional Budget Office calculates the Gini coefficient to estimate the income gap between higher-income and lower-income households.

(A chart capturing this relationship appears in the printable Trends issue.)

However, there are two different measures that are commonly used in this calculation, and they give different answers regarding trends in inequality.

One is so-called вҖңmarket incomeвҖқ based on pre-tax numbers and the other is вҖңincome after taxes and transfers.вҖқ

For measuring inequality, income after taxes and transfers is the only metric that makes sense.

Unlike market income, income after taxes and transfers is a comprehensive measure of living standards which considers the impact of taxes and social safety net transfers on peopleвҖҷs real economic well-being.

Based on income after taxes and transfers, inequality increased 7 percent in the 30 years from 1990 to 2019.

However, the entire rise occurred from 1990 to 2007. On the other hand, inequality decreased by 5 percent since 2007 when political and media attention to inequality peaked in response to the Great Financial Crisis and the Occupy Wall Street protests.

In short, U.S. income inequality has actually been shrinking over the past 16 years.

Another popular assumption is that вҖңcurrent debt levels are unmanageableвҖқ and this will lead to catastrophic problems in the years ahead.

Do the facts support this assertion?

Let us first consider the state of U.S. household balance sheets.

Private sector net worth now stands at a record $154.3 trillion, al most double what it was just 10 years ago.

Even after adjusting for inflation, we find that the net worth of U.S. households has been increasing at an average rate of 3.6% per year since 1952.

That works out to a 12-fold increase in just 70 years.

Critics would say, вҖңthe population has also increased a lot over that same period.вҖқ

However, if we look at inflation-adjusted per capita data, we find that the living standards of the average American have increased by a factor of almost 6 in the past 73 years.

On the other hand, itвҖҷs outrageous that our Federal debt as a percentage of GDP is roughly 124%.

However, itвҖҷs worth noting that this figure previously soared to 119% at the end of World War II, just as the great post-war boom was about to begin.

From there, it fell to a low of about 32% in the mid-1970s and rose to just over 55% in 2001.

The current peak developed in the wake of stimulus related to the Great Financial Crisis and the Covid pandemic.

While 124% is high, that debt has only become risky since the Federal Reserve recently raised rates, driving up the governmentвҖҷs debt service costs.

And even then, only about 23% is owed to non-U.S. entities, so it simply provides a risk-free place for U.S. citizens, companies, and agencies to park their money.

More importantly, because this debt is denominated only in U.S. dollars, the Federal government does not face the default risk most other countriesвҖҷ face with their sovereign debt.

Furthermore, AmericaвҖҷs economic and geopolitical advantages, mean that its GDP is likely to grow faster than government debt in the decades ahead, bringing this ratio down.

On the other hand, the private sector does have a non-zero chance of insolvency or default at some point.

But the good news is that the private sector has de-leveraged by about 40% since 2007!

That means private sector debt as a percentage of GDP is now back down to where it was in the early 1970s.

Based on the foregoing, there is little, if any, reason to worry about U.S. debt levels.

Nevertheless, we need to avoid borrowing to fund counter-productive priorities.

Next, letвҖҷs consider whether вҖңthe link between productivity and worker pay is broken.вҖқ

The simple answer is вҖңNo! It isnвҖҷt.вҖқ

You might have seen some version of the chart in the printable issue titled, вҖңHourly Wages and Output per Hour.вҖқ

It shows a massive long-term divergence of five-to-one between productivity growth and wage growth.

However, this chart is highly misleading.

In a recent research paper titled вҖңThe Link Between Productivity and Wages Is StrongвҖқ Michael R. Strain of the American Enterprise Institute focuses on another chart which tells a radically different story about productivity and pay.

It shows that productivity growth and wage growth move together decade-after-decade.

Here we see some modest divergence since 2000, but nothing like the disconnect seen in the first chart.

The fact is the second chart more accurately reflects economic reality in its basic conceptual choices.

First, it defines output as net output rather than gross output.

Productivity calculated based on net output per hour of work makes sense since it removes capital depreciation.

As Strain observes, вҖңSince depreciation is not a source of income, net output is the better measure to use when investigating the link between worker compensation and productivity.вҖқ

Second, itвҖҷs better to include non-wage compensation, including health benefits, rather than just wage compensation given that non-wage compensation has risen as a share of total worker compensation.

In contrast to the current narrative in some policy circles, this analysis makes clear that the link between productivity and wages remains strong.

As a result, there is little reason to argue that American workers, on average, are being short-changed relative to their contribution to the system.

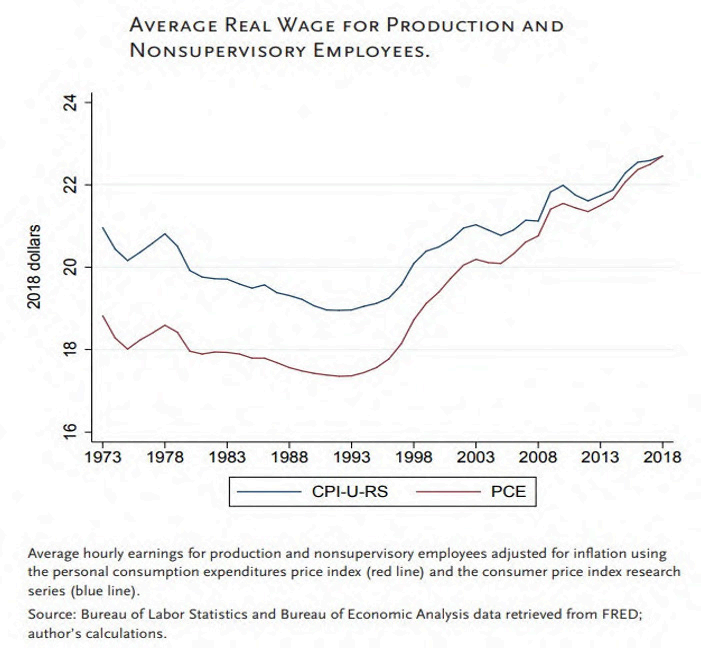

Another popular canard is that Worker wages have gone nowhere for decades.

The most common version of this claim is that вҖңsince the 1970s, real wages havenвҖҷt gone up much at all.

In fact, some pundits argue that wages may have only risen 5% over the past five decades of American economic history.

And this leads to a highly misleading claim of widespread вҖңstagnation.вҖқ

The truth is that, from the peak of the 1990 business cycle through 2019, real wages have actually gone up by 20% as measured relative to the consumer price index and by over 33% as measured relative to the price consumption expenditure (or PCE) index, according to StrainвҖҷs calculations.

Moreover, if we consider how much money peo ple have after taxes and transfers, the stagnation argument looks even more dubious.

Consider five key facts the CBO noted in its recent look at incomes from 1979 through 2019:

First, over the 41 years, every income group saw its highest average вҖңincome after transfers and taxesвҖқ in 2019.

Second, income growth after transfers and taxes was fastest for top earners; however, it was pretty comparable across the entire distribution due to progressive taxes and safety net transfers.

Third, after transfers and taxes, the lowest quintileвҖҷs income grew 94 percent – or 1.7% annually.

Fourth, after transfers and taxes, the middle three quintilesвҖҷ income grew 59 percent – or 1.2 percent annually. And,

Fifth, after transfers and taxes, the highest quintileвҖҷs income grew 123 percent or 2.0 percent annually, reaching $252,100 in 2019 versus $113,100 in 1979.

An important factor was that the average federal tax rate for top earners decreased, resulting in slightly faster growth in income after taxes.

And that brings us to the nearly ubiquitous claim that upward mobility is a thing of the past.

The truth is that upward mobility is still happening. But itвҖҷs less obvious than it was 50-to-100 years ago.

To understand, ask yourself, вҖңAre people doing better in their 40s than their parents were doing during their 40s?вҖқ

Overall, research shows that around 73 percent of Americans in their 40s have higher real incomes than their parents did.

And for kids raised in the bottom 20 percent, that number is 86 percent.

However, it has become less likely that someone will be able to move up from a lower quintile to a higher quintile.

ThatвҖҷs different than simply being better in absolute terms.

As explained in prior Trends issues, much of this difference is due to a divergence in lifestyle attributes between people born into the five income quintiles.

For example, research from the Brookings Institution shows that graduating from high school, getting and keeping a job, staying out of jail and not having a child until married can virtually ensure a life free from poverty.

Beyond those metrics, having two parents at home correlates strongly with upward mobility.

However, those are values not often mimicked by friends and family in the bottom two economic quintiles.

The influence of peers largely explains why those at the bottom disproportionately stay at the bottom, while the same is true for the top.

WhatвҖҷs the bottom line?

The foregoing analysis demonstrates that things are better than most Americans and economic pundits believe.

However, things could be better still. Investors, managers, and policy-makers must remain vigilant if we hope to make things even better for ourselves and future generations.

Given this trend, we offer the following forecasts for your consideration.

First, in the coming decade, real U.S. economic growth will return to the 3.1% trend it enjoyed prior to the Great Financial Crisis.

This will be made possible by the AI-driven productivity revolution described in trend #2, coupled with talent migration discussed in trend #4.

Second, the biggest threat to AmericaвҖҷs coming resurgence involves the continued regulatory overreach discussed in trend #3.

Resources now devoted to compliance with obsolete and counter-productive regulations will be reallocated to productivity enhancing priorities.

This should quickly eliminate the cumulative regulatory drag on economic growth over the past 40 years raising GDP growth rates by at least 1% a year, in perpetuity.

Third, North AmericaвҖҷs growth will benefit enormously from todayвҖҷs global demographic crisis during the 2020s.

The new Cold War will increasingly limit the global flow of resources and technologies, creating a powerful down-draft for economies in the de-facto Sino-Russian alliance.

Meanwhile, the workforce in most European and Asian countries is rapidly aging and shrinking limiting their growth possibilities.

So, as re-shoring and friend-shoring accelerate, the вҖңbest and the brightestвҖқ will be drawn to where they see the most upside and that will typically be North America.

Since, assimilation is a key competitive advantage of the United States and Canada, they will be able to take advantage of the worldвҖҷs increasingly mobile talent pool as explained in trend #4.

Fourth, absolute income inequality is likely to increase slightly as a premium is placed on talent and merit.

However, the shortage of skilled blue-collar talent means that percentage gains will be greatest in those job categories.

Fifth, as the AI-driven productivity boom takes off, the national debt will shrink as a percentage of GDP.

This surge in GDP will increase tax revenues reducing the deficit.

And as we saw in the 1990s, a tech driven boom may even create a budget surplus.

Combined with lower interest rates, these factors will make servicing the national debt easier than it is today. And,

Sixth, total worker compensation will continue to keep pace with productivity, even as profit margins in most industries expand.

Because of the increased contribution of technology to profits, shareholder returns will accelerate.

However, these gains will not come at the expense of workers.

Resource List

1. Faster, Please! September 4, 2023. JAMES PETHOKOUKIS. What is the outlook for long-term US economic growth?

2. Seeking Alpha. August 30, 2023. Scott Grannis. Is This A Great Country Or What?

3. Seeking Alpha. August 30, 2023. Scott Grannis. 2% Growth And 2% Inflation: The FedвҖҷs Done.

4. Faster, Please! August 21, 2023. JAMES PETHOKOUKIS. Four shocking truths about the American economy! (Well, shocking to some.)

5. Trends. October 11, 2014. Trends Editors. AmericaвҖҷs Slow, Painful Techno-Economic Transition.